STOP GETTING RORTED BY YOUR HOME INSURANCE PREMIUMS

How To Slash Your Home & Contents Insurance By 30-60% And Keep It Down Year After Year In Just 72 Hours

(even if you've already shopped around and "there's nothing cheaper out there")

The Proven System That's Helping Australian Homeowners Break Free From The Annual Premium Nightmare

"I'm sick of being treated like a mug

by these insurance companies."

Does this sound familiar?

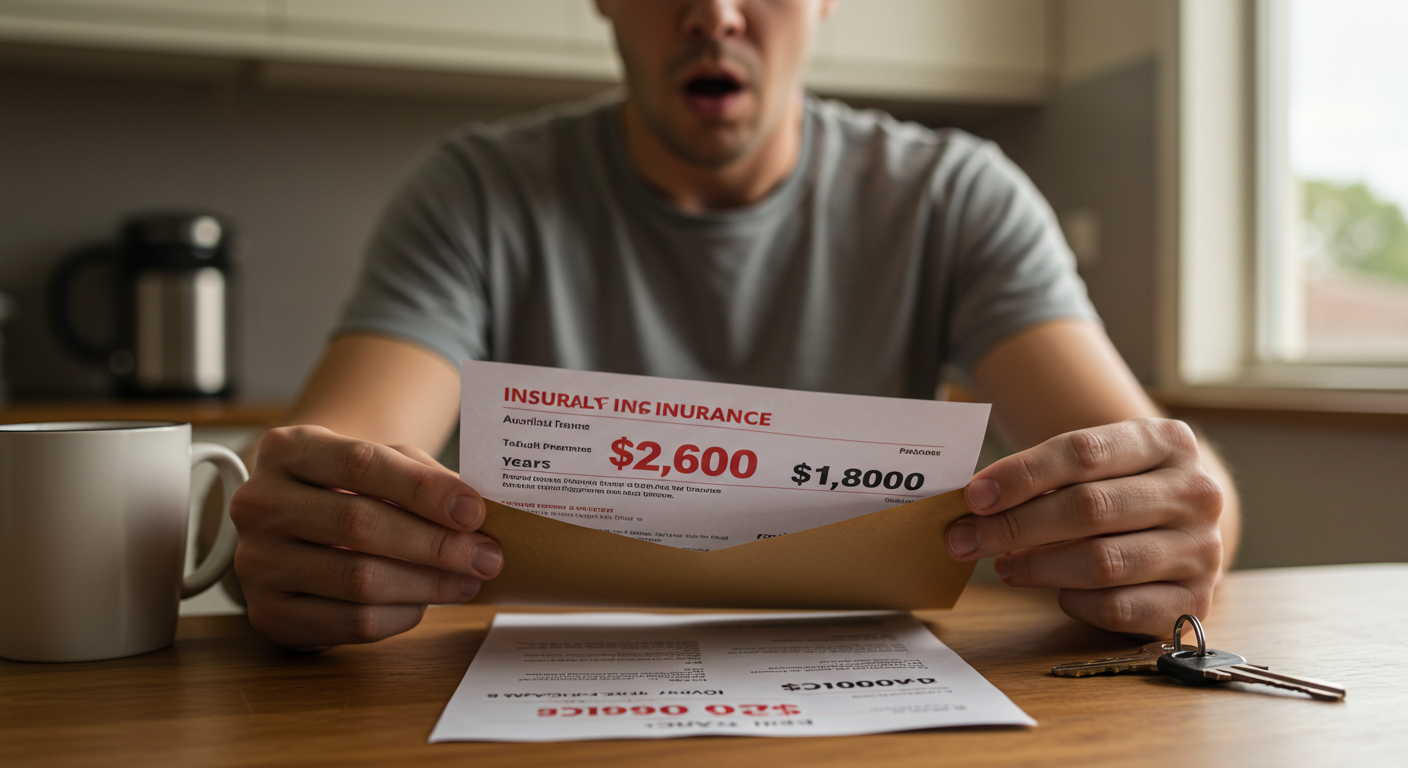

You open your renewal notice and your stomach drops. Again.

Your premium's jumped another $800. No claims. No changes. No explanation that makes any bloody sense.

Last year it was $1,800. Now they want $2,600. The year before that? $1,300.

Where does it end?

Now your daily struggle with home insurance includes:

Spending hours every year comparing quotes online - only to find every insurer is within $100 of each other, and none of them are anywhere near what you were paying two years ago

Getting wildly different quotes for the exact same property - AAMI wants $6,000, Allianz wants $2,500, and you're left wondering if you're being scammed or if they actually know something about your property you don't

Being told you're "high flood risk" when you live on a bloody hill - meanwhile your neighbors down the street somehow got coverage for half what you're paying

Calling to complain and being told to "shop around if you don't like it" - by customer service reps reading from scripts who couldn't care less that you've been a loyal customer for 8 years

Watching your premium climb 30-50% year after year - while your salary definitely hasn't, and every other bill is going up too, and you're starting to wonder if you can even afford to own a home anymore

You've tried everything the "experts" suggested:

Increasing your excess to $2,000 (which barely knocked $200 off your premium and now you're terrified to actually claim anything)

Bundling with your car insurance (which somehow made both premiums go up when you added them together)

Using comparison websites religiously every renewal (only to waste 6 hours getting nearly identical quotes that are all 40% higher than last year)

Calling your insurer to "negotiate" (and being told there's nothing they can do, take it or leave it)

Removing flood cover to save money (even though you need it, because what choice do you have?)

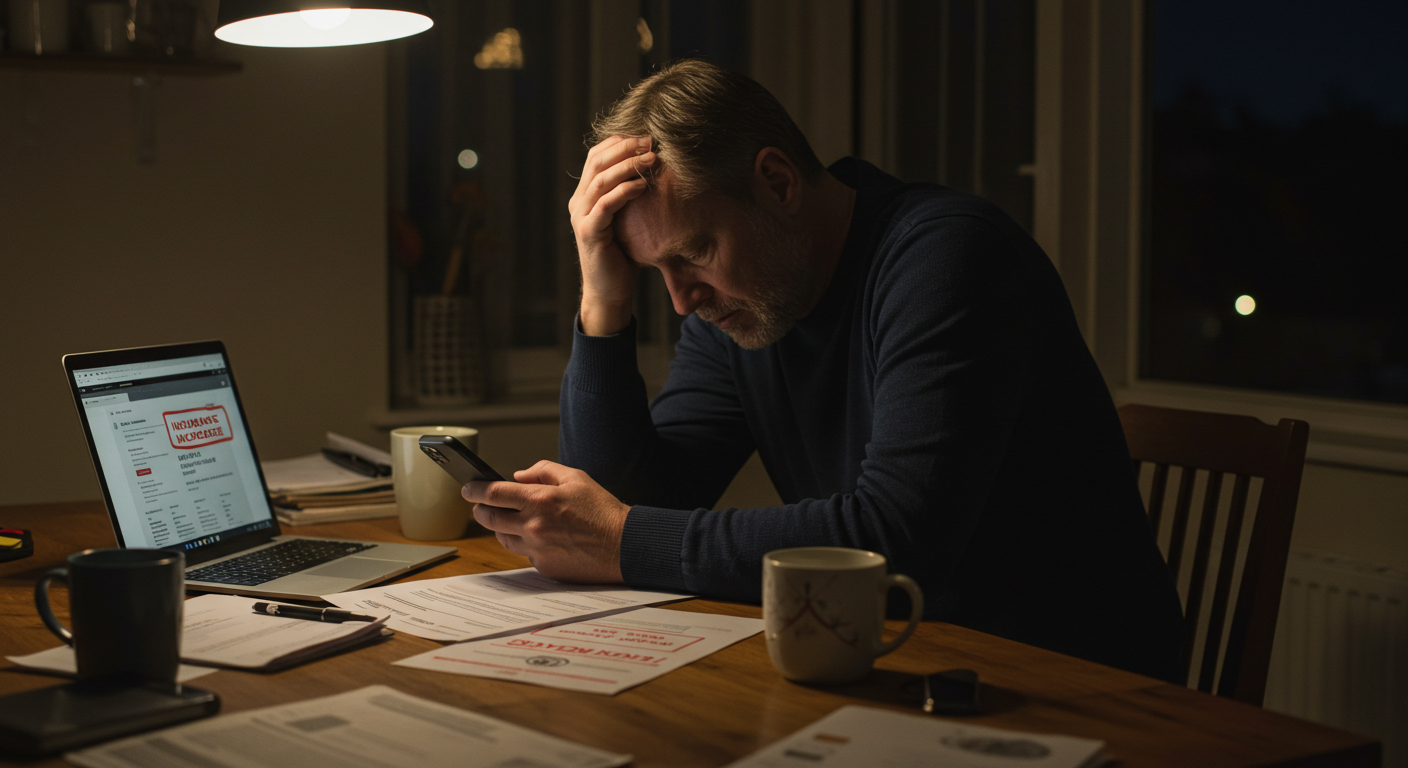

And you're left feeling completely helpless.

Then I Discovered Something That Changed Everything...

My name Is Nick Ferrier, but that's irrelevant - what matters is I'm an Australian homeowner just like you, and I was paying $4,200 a year for home and contents insurance on a modest 3-bedroom brick home in suburban Brisbane.

No pool. No flood history. Nothing fancy.

When my premium jumped to $5,800 in one renewal, I'd had enough.

This is what shocked me when I started digging:

Insurance companies use over 200 risk factors to price your policy - and most Aussie homeowners are unknowingly triggering the expensive ones without realizing there are legitimate ways to address them

Your postcode alone can add $1,500 to your premium - but there are specific ways to demonstrate your individual property's lower risk that most homeowners never learn about

The average Australian homeowner is overinsured by 15-40% - paying for rebuild costs that are inflated by $100,000-$300,000 beyond what they'd actually need

Most policies include 6-12 "extras" you never asked for - like accidental damage cover and automatic jewelry cover that's adding $400-$900 to your annual premium

But most alarming of all:

Most Australian homeowners are unknowingly leaving their policy on autopilot - accepting whatever sum insured the insurer suggests, which is often deliberately inflated to maximize premiums, costing them thousands every single year.

I know because I was making all these same mistakes...

Through extensive research and consultation with:

Former insurance underwriters who've worked at the big Australian insurers

Risk assessment specialists who actually set the pricing models

Insurance brokers who've helped thousands of Aussie families slash their premiums

I discovered WHY the annual "shop around" advice fails - and more importantly, what actually works to keep your premiums down year after year..

After going through all of this, year after year, I made this guide…

I call it the "Australian Insurance Premium Defence System"

By understanding exactly how Australian insurers calculate risk, which specific factors you can control, and which levers actually move your premium down (not just sideways), I was able to:

Cut my own premium from $5,800 to $2,100 - with better coverage than before, including flood cover I'd previously dropped

Stop the annual 30-50% increases - by implementing a system that keeps insurers competing for my business on my terms

Identify and eliminate $3,400 of unnecessary coverage - that was padding my premium without providing any real protection

Reduce my rebuild sum insured by $240,000 - after discovering my insurer had it inflated by nearly 40% beyond what I'd actually need

Save over 15 hours per year - by systematizing the entire process so it takes 90 minutes annually instead of weekend after weekend of frustration

After helping 247 other Australian homeowners replicate these results, I've refined this system into a step-by-step method that anyone can use...

...even if you've already shopped around and been told "that's just what it costs now."

But don't take my word for it. Listen to these Aussie homeowners:

THE FACTORS THAT SEPARATE LOW PREMIUMS FROM RIP-OFF PRICING

The 5 Essential Levers

Australian Homeowners Need

(That Comparison Sites Don't Reveal)

LEVER 1: Accurate Rebuild Valuation

- Most insurers suggest rebuild costs 20-45% higher than necessary because it directly inflates premiums. Every $100,000 of unnecessary building cover costs you $120-$200 annually for protection you don't need (and if you're paying for $250,000 you don't need, that's $300-$500 wasted every single year).

LEVER 2: Risk Factor Documentation

- Insurers use algorithmic risk ratings for flood, fire, and storm that often don't reflect your specific property's real risk. Knowing how to properly document and present your property's actual risk profile can reduce premiums by $500-$2,400 annually (and most Aussies have no idea this is even possible).

LEVER 3: Coverage Optimization

- The average policy includes $4,800 of building cover and $600 of contents cover for things you don't need, didn't ask for, and will never claim. Identifying and removing these bloat features takes 15 minutes and saves hundreds annually (and won't leave you underinsured where it matters).

LEVER 4: Strategic Excess Positioning - Most homeowners randomly pick excess amounts without understanding the premium reduction formula. There's a specific excess "sweet spot" for your premium tier that maximizes savings without exposing you to unrealistic out-of-pocket risk (and it's rarely the number insurers recommend).

LEVER 5: Insurer Rotation Strategy

- Staying with the same insurer costs the average Australian homeowner $600-$1,800 annually in "loyalty tax." But switching randomly doesn't help either. There's a specific rotation pattern that forces insurers to compete for your business while maintaining continuous coverage (and it takes 90 minutes once per year).

INSTANT ACCESS - START SLASHING YOUR PREMIUMS TODAY

Here's Everything You Get With The Australian Insurance Premium Defence System Today!

What's included:

The Complete Australian Insurance Premium Defence System:

5 proven modules that eliminate the annual premium nightmare and put you back in control of your insurance costs

🎁 Plus These 3 Essential Bonuses 🎁

BONUS #1: "The Contents Value Reality Check Workbook" - Room-by-room assessment tool that calculates what you actually own and what it costs to replace, preventing the over-insurance trap where insurers suggest $150k contents when you really have $60k worth of stuff (typically reduces contents premiums by $200-$450 per year)

BONUS #2: "The Comparison Leverage Framework" - Step-by-step system for pitting competing quotes against each other to force insurers to compete for your business, including the exact 45-day timeline and "three-quote rule" that gives you maximum negotiating power (saves users $400-$1,600 annually through strategic quote timing and presentation)

BONUS #3: "The Retention Offer Negotiation System" - Word-for-word scripts and proven conversation sequences for unlocking the "retention discounts" insurers reserve for customers who know how to ask, including which competitor quotes to mention and exactly when to negotiate vs. walk away (cuts 15-35% off renewal quotes)

Normally: $97

Today: $27.99

BEFORE AND AFTER

Here's You Can Expect

Don't let insurance companies continue treating you like a cash machine.

Your home insurance can be affordable and fair again - you just need the right system to make it happen.

Before

The Premium Defence System:

Dreading your renewal notice every single year and feeling your stomach drop when you see the new premium

Spending 6-8 hours comparing quotes online only to find they're all within $200 of each other and nowhere near what you used to pay

Feeling completely powerless when insurers hit you with 40% increases and tell you to "shop around" or "take it or leave it"

Wondering if you're being scammed when you get quotes ranging from $2,500 to $8,000 for the same property

Paying for $200,000 of unnecessary building coverage because your insurer suggested it and you didn't know how to verify it

Lying awake at night worried about dropping coverage you need just to afford the premium, or worse, going without insurance entirely

After

The Premium Defence System:

Confidently knowing your premium is fair, accurate, and reflects your property's actual risk - not inflated algorithmic guesswork

Having insurers compete for your business on YOUR terms, using leverage and documentation they can't dismiss or ignore

Spending 90 minutes once per year on insurance (with a clear checklist) instead of endless frustrated hours getting nowhere

Slashing your premium by 30-60% while maintaining or even improving your coverage where it actually matters

Keeping your premiums stable year after year by implementing the rotation strategy that prevents loyalty tax creep

Never feeling ripped off again because you'll know exactly what you're paying for and why

YOUR PREMIUM REDUCTION PATH BEGINS HERE

The 5 Modules That Will

Transform Your Insurance Costs:

Each module precisely designed to tackle one specific premium inflation tactic through proven Australian-specific strategies.

MODULE 1: The Rebuild Reality Check (Complete in 45 minutes)

Finally know your home's accurate rebuild cost - this systematic assessment helps you identify overinsurance while ensuring you're never actually underinsured where it matters.

The 3-factor formula that determines your TRUE rebuild cost (not the inflated number insurers suggest)

How to account for your home's age, construction type, and regional building costs accurately

The free online tools (specific to Australia) that verify your calculations and give you documentation insurers accept

MODULE 2: The Risk Rating Reversal (Complete in 60 minutes)

Stop paying for risk you don't actually have - our documentation method helps you properly present your property's real risk profile while building an evidence file insurers actually review.

Which specific photographs and measurements to take that demonstrate lower flood/fire/storm risk

The exact format insurers prefer when reviewing risk documentation (wrong format gets ignored)

How to obtain council flood studies and independent risk assessments that support premium reductions

MODULE 3: The Coverage Audit Checklist (Complete in 30 minutes)

Identify every dollar of unnecessary coverage - our line-by-line audit helps you strip out profit-padding extras while keeping coverage that actually protects your financial security.

The 11 most common coverage add-ons that inflate premiums $400-$900 annually (and when you actually need them vs. when they're wasted money)

How to calculate your TRUE contents value using the room-by-room method that prevents overinsurance

Why "total replacement" building cover costs 40% more than "sum insured" but usually offers zero additional protection

MODULE 4: Strategic Excess Optimization (Complete in 20 minutes)

Find your perfect excess amount - our calculator helps you balance premium savings against realistic out-of-pocket risk using your specific financial situation and claim probability.

The premium reduction formula that shows exactly how much each excess increase saves (it's not linear)

Why the "$1,000-$2,000 range" advice is wrong for 60% of homeowners (and how to find YOUR number)

How to set different excesses for building vs. contents vs. specific risks to maximize savings where it matters

MODULE 5: The Rotation Strategy Blueprint (Complete in 90 minutes annually)

Stop paying loyalty tax forever - our proven rotation system helps you systematically switch insurers every 2-3 years while maintaining continuous coverage and creating competitive pressure.

The exact 45-day timeline that forces insurers to compete (starting earlier or later reduces leverage)

Which Australian insurers actually price new customers fairly vs. which ones will sting you in year 2

How to maintain claim history and no-claim bonuses when switching (avoiding the "new customer" penalty)